CHI’s health reform “strike team,” a group of analysts from across our organization with different areas of expertise, delved into the proposed Better Care Reconciliation Act (BCRA) to provide an early determination of its potential impact on Coloradans.

Our estimates and predictions will be updated if, as expected, details of the proposal change between now and the vote of the full Senate.

The analysis found that the BCRA would have the biggest impact on the Medicaid program, which now covers one of every four Coloradans. Colorado lawmakers would be handed a bigger bill for Medicaid, leading to some tough choices. At the same time, the law would give states more latitude in designing health policy.

In any case, CHI expects that the state’s uninsured rate, which fell to a historic low of 6.7 percent in 2015, will begin to head higher.

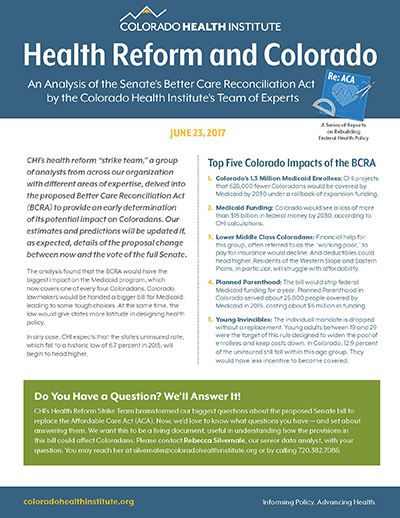

Top Five Impacts of the BCRA

- Colorado’s 1.3 Million Medicaid Enrollees: CHI projects that 628,000 fewer Coloradans would be insured by 2030 under a rollback of Medicaid expansion funding.

- Medicaid Funding: Colorado would see a loss of more than $15 billion in federal money by 2030, according to CHI calculations.

- Lower Middle Class Coloradans: Financial help for this group, Often referred to as the “working poor,” to pay for insurance would decline. And deductibles could head higher. Residents of the Western Slope and Eastern Plains, in particular, will struggle with affordability.

- Planned Parenthood: The bill would strip federal Medicaid funding for a year. Colorado Planned Parenthood served about 25,000 women covered by Medicaid in 2015, costing about $6 million in funding.

- Young Invincibles: The individual mandate is dropped without a replacement. Young adults between 19 and 29 were the target of this rule designed to widen the pool of enrollees and keep costs down. In Colorado, 12.9 percent of the uninsured still fall within this age group. They would have less incentive to become covered.

CHI’s Experts Answer Frequently Asked Questions

Medicaid

Emily Johnson, Senior Policy and Statistical Analyst

Emily Johnson, Senior Policy and Statistical Analyst

Question: Of the 1.34 million Coloradans covered by Medicaid, how many may lose their coverage? What do we know about them?

Answer: The BCRA would make it nearly impossible for Colorado to maintain Medicaid expansion because it would greatly reduce the federal funds received by expansion states. By 2030, we project that 628,000 fewer Coloradans would be insured through Medicaid than would have been under the ACA – more than a third of all enrollees.

Most of these would be low-income adults without dependents. Some low-income parents would be affected as well.

Question: Will Colorado see a cut in federal funding for Medicaid? If so, how much and over what time? How did you reach this conclusion?

Answer: Yes, Colorado would receive less federal funding under the BCRA. This is by design. A major goal of this legislation is to reduce federal spending.

The differences would start small but grow fast. By 2024, the state would expect federal Medicaid funding to decline by more than $1 billion annually. This would total more than $15 billion over the first 10 years of the BCRA

There are two main ways the BRCA would reduce federal Medicaid funding. The first is through a gradual reduction of the enhanced federal payment for Medicaid expansion enrollees. The second is through a new funding mechanism called “per capita caps,” which would provide the state a set amount per enrollee. This allotted amount would grow by the medical care inflation rate for the first few years of the law, and overall inflation after that. Any Medicaid costs above this amount would fall squarely on the Colorado state budget.

CHI developed a statistical model to project Medicaid enrollment and annual per capita costs under this scenario. We relied on the text of the BCRA and historical data on Medicaid spending, enrollment, and other economic trends to arrive at our projections.

Question: How does this compare to the House AHCA bill?

Answer: In terms of federal funding for Medicaid, the impact of the House and Senate bills between 2020 and 2030 don’t differ by much. CHI estimates the AHCA would result in $14 billion in lower federal funding over this period versus $15 billion in the BCRA.

However, the timing of the funding cuts is different. Funding would be higher under the BCRA than the AHCA until 2024. From 2024 on, BCRA funding would be lower than the AHCA. This would remain the case in the very long term, past 2030.

A similar phenomenon happens in terms of coverage. In both bills, about a third of Medicaid enrollees are projected to lose coverage by 2030. However, in the AHCA this happens gradually. In the BCRA, expansion funding rates begin to be rolled back 2021, reaching traditional funding rates by 2024.

Question: Are there some counties that will be impacted more than others by a loss of coverage?

Answer: The only enrollees at risk of losing coverage are those covered under the ACA’s Medicaid expansion. Therefore, the greatest impact will be on communities with higher rates of Medicaid expansion enrollment.

In many urban, higher-income counties such as Douglas and Broomfield less than five percent of the population is covered through Medicaid expansion. But for some rural parts of the state — most notably, the San Luis Valley and southeastern corner of Colorado — 15 percent of residents rely on Medicaid expansion. In Costilla county, one of every five residents stand to lose Medicaid coverage under the BCRA.

In general, a higher percentage of residents would be affected in rural counties than Colorado’s urban centers.

Question: With your expectation that Colorado would receive less federal funding for Medicaid under the new law, what options would the state have when it comes to sustaining the program and caring for enrollees?

Answer: There are four main options for Colorado’s Medicaid program if faced with these cuts.

First, the state could cut back on the number of people covered. In all likelihood, this would be the state’s response to the reduced federal match for Medicaid expansion enrollees. But the state would also get less money per non-expansion enrollee, so ending coverage for Medicaid expansion enrollees alone won’t make up for the $15 billion funding gap.

A second option, then, would be to change the benefits of the Medicaid program. For example, the state could choose to cover fewer services or ask enrollees to pay for a larger portion of the cost of their care.

Third, the state Medicaid program could reduce provider reimbursements for services. However, this does risk having fewer providers accept Medicaid, and therefore could limit enrollees’ access to care.

Finally, the state could find new and innovative ways to save money in the program without changing benefits, enrollment or provider payments. Managed care has often been cited as a possible approach for cost-savings in Medicaid, but the evidence to back this up is mixed. The state Medicaid department may also be able to find some administrative savings, but it already operates with very low overhead so the potential of administrative savings is limited.

Colorado would likely have to adopt one or more of these approaches.

Coloradans Who Buy Insurance Through Connect for Health Colorado

Edmond Toy, Director

Edmond Toy, Director

Question: How will the new law change who get subsidies to purchase insurance? Which Coloradans may get higher subsidies? Which Coloradans may get lower subsidies?

The Senate bill maintains some elements of the ACA’s subsidies for people to buy insurance on the individual market. Although it is more generous than the House’s plan, the Senate bill probably reduces the availability and size of the subsidies that are currently available in the Affordable Care Act (ACA).

Under the ACA, two types of financial assistance are available for people who purchase insurance plans through Colorado’s health insurance exchange, Connect for Health Colorado. First, people are eligible to receive tax credits to help them pay the premiums. The exact size of the tax credit depends on income, and it is available for people with incomes up to 400 percent of the federal poverty level. Greater tax credits are also available in areas with more expensive insurance premiums. The average tax credit in Colorado is about $4,400 per year, according to Connect for Health Colorado. In some high-cost areas of Colorado, though, the average subsidy is much higher. For example, in Delta County, the average tax credit is nearly $9,800.

Second, people with incomes between 100 and 250 percent of the federal poverty level are eligible for cost-sharing subsidies. These subsidies reduce the out-of-pocket costs (e.g., co-payments and deductibles) that people pay when they receive health care services.

So how does the Senate bill change the subsidies?

First, tax credits would still be available to help people pay their insurance premiums, but the scope of the tax credits are different. The income cutoff for who is eligible to receive tax credits would be reduced from 400 percent of the federal poverty level to 350 percent. This contrasts with the House plan, which did not base tax credits on income.

The Senate also proposes to base the size of the subsidy on the cost of insurance. This is how the ACA is structured, but was absent in the House plan. This means that areas with more expensive insurance would be eligible for greater tax credits, which is good news for people who live in the mountain and rural areas of Colorado where insurance premiums tend to be higher. Nevertheless, we still expect that the subsidies in the Senate bill will be lower than what is available in the ACA.

Second, the Senate bill eliminates the cost-sharing subsidies that were targeted at people with lower incomes (up to 250 percent of the federal poverty level in the ACA).

Together, these provisions will reduce the subsidies available in the ACA, but it seems to respond to President Trump’s recent calls for subsidies that are more generous than the House plan.

Opioid Epidemic Funding

Tamara Keeney, Policy Analyst

Tamara Keeney, Policy Analyst

Question: Does the BCRA include funding to address the opioid epidemic?

Answer: The Senate bill appropriates $2 billion in fiscal year 2018 for state grants to support treatment and recovery support services for people with mental or substance use disorders. This proposed amount is far less than the $45 billion requested by senators from two states hit hard by the opioid epidemic, Ohio and West Virginia.

Critics argue that the $2 billion is not nearly enough to make up for the changes to Medicaid funding and cuts to the Medicaid expansion. In 2015, nearly 30 percent of Colorado’s 880 overdose deaths were Medicaid clients. Medicaid covers addiction recovery services and medications such as Suboxone. In addition to behavioral health services, Medicaid covers the primary care that members use to maintain the other parts of their health care. The bill does not discuss funding after 2018.

Stabilizing the Insurance Market

Alex Caldwell, Policy Analyst

Alex Caldwell, Policy Analyst

Question: What options are included to help Colorado stabilize its insurance markets?

Answer: Both the House bill and the Senate bill include more than $100 billion in funding between 2018 and 2026 to help states stabilize their individual markets. States could consider high-risk pools, reinsurance schemes, or other programs that help high-risk patients afford care, such as co-payment subsidies.

But one difference is that the Senate’s bill directs a lot of that money to insurers rather than the state. It’s a type of reinsurance program, and states don’t need to match those funds. The rest of the money goes directly to states, and there is a matching requirement.

Not only does the Senate’s bill send less money directly to states, it also gives less spending flexibility to the states. The AHCA is more flexible, allowing states to spend the money on things like maternity care, prevention, and early detection of mental illness.

Question: The AHCA and the BCRA both provide funding to help cover people with pre-existing conditions, with high-risk pools being one option. What is Colorado’s experience with high-risk pools

Answer: Colorado has experience with two high-risk pools — CoverColorado, which was run by the state, and another run by the federal government during the transition period before implementation of the ACA.

Both offered insurance to people with pre-existing conditions who didn’t have another option in the pre-ACA world, when insurers could refuse to cover them. But both were very expensive. The federal pool closed a year early with a $2 billion shortfall nationally. CoverColorado cost almost $160 million at its peak of 14,000 members in 2012, and it required other revenue to stay afloat, including assessments on insurers and money from the sale of abandoned properties.

If Colorado’s history is a lesson, high-risk pools need substantial funding.

But under the ACHA, Colorado’s 2018 share of the funding would be about $255 million, even though a high-risk pool opened today in Colorado could cost as much as $615 million to run for one year. That’s based on an estimated number of enrollees multiplied by CoverColorado’s per capita costs, then adjusted up for medical inflation.

The price tag would depend on a slew of factors – who would be eligible, who would opt in, how expensive the care is for those enrollees, premium caps, benefit packages and limitations, and availability of external sources of state or federal funding. Federal funding and premiums could cover some of that, but the state would be on the hook for the rest. Regardless, the price tag would be significant and challenging for states to predict.

Premium Pricing Changes Based on Age

Ian Pelto, Research Analyst

Ian Pelto, Research Analyst

Question: Will older Coloradans face higher premiums? How many younger Coloradans may see their premiums fall? Do states have options to address the potential need to help older Coloradans afford insurance?

Both the House and Senate bills would change the insurance premium age-rating ratio from 3:1 to 5:1. This change would mean insurers could charge an older person up to five times what they would charge a younger person. In other words, younger Coloradans would likely see a drop in their premiums.

A study by the RAND Corporation estimates that an average 21-year-old’s premiums would decrease by 25 percent, or $720 per year. At the same time, a 64-year-old’s premiums would rise by about 25 percent, or about $2,090 per year. This does not account for the dramatic differences in premiums across Colorado, and some older Coloradans could see even steeper price increases.

Of the 330,000 Coloradans with individual insurance, 25 percent are between 55 and 64 and would see the greatest increase in premium prices. About 28 percent are between the ages of 18 and 34, and would see the greatest decreases in their premiums.

The AHCA would have allowed the state to change the age-rating ratio. The Senate version does not make that allowance.

Essential Health Benefits

Joe Hanel, Manager of Public Policy Outreach

Joe Hanel, Manager of Public Policy Outreach

Question: Will the insurance plan benefits that were required under the ACA, known as the essential health benefits, change in Colorado?

Answer: Both the Senate and House bills allow states to waive the ACA’s essential health benefits. We think Colorado would not apply for this waiver under the state’s current political leadership. Historically, the legislature has adopted relatively strong mandates for insurance companies to cover certain conditions — under both political parties. A 2009 study (from before the ACA) showed Colorado had 51 coverage mandates in law, ranking 15th among the states for the number of essential health benefits it requires insurers to cover.

Most of these benefits remain in state law, so even if the ACA’s essential health benefits were waived, Colorado would have a fairly strong — but different — set of health benefits. These state-mandated benefits include (to name a few) coverage for pregnancy and childbirth, contraception, mental illness, preventive health screenings, and a long list of benefits for children, including autism treatment.

Coloradans Who Purchase Their Insurance Through Their Employer

Edmond Toy, Director

Question: Will the AHCA affect people who get their health insurance through their employer?

The Senate bill will not change very much for workers who get insurance through their employer (employer-sponsored insurance, or ESI). In Colorado, 57 percent of people under the age of 65 get insurance through ESI, making it the main source of health coverage.

Although much of the health care debate as focused on Medicaid and subsidies for people who buy insurance on the individual market, federal policy has a big impact on ESI. Under long-standing tax laws, workers’ health insurance benefits are not taxed like regular income. This tax structure acts like a subsidy because it reduces the effective price of workers’ health insurance. Reducing or eliminating the ESI tax subsidy would effectively raise the cost for workers to get insurance, but it would also mean the federal government would collect more tax revenue that could help pay for other parts of health care reform.

At various times, Republicans have floated proposals to make substantial changes to ESI. Last year, Congressman Paul Ryan proposed to limit the ESI tax subsidy. Although both the House and Senate reportedly considered reducing or eliminating the tax subsidy, those proposals did not survive, and the current policy for ESI largely remain intact.

One exception relates to the so-called “Cadillac tax.” This refers to a provision in the ACA that limited the ESI tax subsidy by imposing a tax on ESI plans that were very generous. This provision was unpopular among labor unions because some of their members would be subjected to the Cadillac tax and among fiscal conservatives who want to reduce taxes. Since the passage of the ACA, Congress has delayed the implementation date of the Cadillac tax, and the Senate bill prohibits the Cadillac tax from taking effect until 2025.

Medicare and Aging

Teresa Manocchio, Policy Analyst

Teresa Manocchio, Policy Analyst

Question: Will Coloradans covered by Medicare see any changes resulting from the new bill?

Answer: No, the bill does not propose any direct changes to Medicare benefits, so Coloradans who rely solely on Medicare for their health coverage will not see any changes.

However, the proposed cuts to the Medicaid program will impact seniors who are eligible for both Medicare and Medicaid. The Senate bill also repeals two high-income Medicare taxes which have long-term implications for the sustainability of the Medicare program – and that would almost certainly impact Medicare benefits in the future.

Question: To what degree could Medicaid cuts affect Colorado seniors?

Options to manage state Medicaid spending under the AHCA’s “per capita caps” include covering fewer people or covering fewer services – or both. Low-income seniors who are eligible for both Medicaid and Medicare are particularly vulnerable, because they rely solely on Medicaid for long-term services and supports. Many of these supports, such as home and community based services, are benefits that the state is not required to cover and may have to reduce or eliminate to continue funding required services.

Public Health Programs

Teresa Manocchio, Policy Analyst

Question: How will the BCRA impact public health funding in Colorado?

Answer: The BCRA repeals the Prevention and Public Health Fund, which was created to support public health programming across the country. Colorado received $9 million from the fund in 2016 and $57 million since the inception of the fund.

More than half of Colorado’s funding for public health activities comes from the federal government. The dollars from the fund support chronic disease prevention, health promotion and epidemiology and infectious disease activities such as suicide prevention, low- or no-cost vaccines for children and food and water testing. Without the support of the fund, Colorado would have to find additional funding to backfill these critical public health activities.

Planned Parenthood

Adrian Nava, Research Analyst

Adrian Nava, Research Analyst

Question: How will the BCRA affect Planned Parenthood funding in Colorado?

Answer: The bill restricts states from making payments to Planned Parenthood. This prohibition will primarily impact the 25,000 or so Coloradans covered by Medicaid who received care at Planned Parenthood in 2016.

Medicaid clients made up about 35 percent of the approximately 70,000 Coloradans who received services at Planned Parenthood in that year.

Medicaid reimbursements amounted to about $6 million in 2015, according to Planned Parenthood.